[ad_1]

The cryptocurrency market has collapsed within the second quarter of 2022, and it might have been foreseen. Warning indicators had been there, however not everybody was conscious of them. When you will have an over-leveraged market that’s going lengthy on crypto costs, when the sudden strikes, there isn’t a approach round it. The Russia/Ukraine battle, provide chain scarcity points, inflation, and rising rates of interest have performed a component within the collapse. What occurred was the results of macroeconomic occasions which have led to financial downturns all over the world.

Whereas the standard monetary markets have been affected severely, this has sadly additionally affected crypto. Bitcoin has fallen considerably, touching beneath $20K, and has been down for 9 consecutive weeks, which was unprecedented. The second high crypto, Ethereum, has additionally fallen and reached beneath the $1K assist degree. The altcoin market was a lot worse in the course of the crash, as promote offs plunged cash like ADA, XRP, BNB, and rising crypto like SOL, AVAX, and DOT. This has introduced the general cryptocurrency market cap beneath $1 Trillion (supply CMC).

The dominoes started to fall in crypto after Bitcoin couldn’t maintain its assist, because it continued falling from $30K between March and Could. The chaos has brought on FUD available in the market as promote offs started. It was additionally a results of adverse information from the Feds rising rates of interest by 25 bps (Beginning in March 2022). This was additional aggravated by rising inflation, reaching 8.6% by Could 2022. This has considerably affected a sector of the crypto business referred to as CeDeFi. Earlier than we get to that, allow us to have a look at the distinction between decentralization and centralization.

The primary function of cryptocurrency is to introduce a decentralized financial system that’s not managed by the federal government. Bitcoin is the very best instance in the meanwhile, because it stays, for essentially the most half decentralized as a result of there isn’t a majority entity or particular person who controls the community. That is in distinction to banks and different monetary establishments, that are extremely centralized.

Centralization means management by an authority that regulates and manages the distribution of forex. The federal government run Central Financial institution is an instance of this (e.g. US Federal Reserves). Every nation has the equal of a central financial institution that points the nationwide forex, which is authorized tender for funds and exchanges. The central financial institution controls the provision of cash via quantitative measures. This sort of management is the other of decentralization. In a decentralized system, the provision of cash is mounted and its worth is decided by the free market.

The rise of DeFi (Decentralized Finance) aimed to deliver extra monetary inclusion and independence to customers. This led to protocols, that are software program developed to offer DeFi companies to customers. The early DeFi protocols had been actually decentralized, that means they’d no organized entity and had been open to all customers. They had been cumbersome and moderately troublesome to make use of, requiring customers to have a point of technical data. This was the place CeDeFi enters the scene.

The rise of CeDeFi begins with digital exchanges like Coinbase and Binance. These firms provide a gateway to crypto as an onramp to onboard new customers. In addition they simplify the method of proudly owning crypto via an expert service that handles the complexities concerned in crypto (e.g. pockets tackle, non-public keys, and so on.). Customers join with these exchanges by present process a KYC course of much like different conventional finance companies. Private info is collected to adjust to anti-money laundering legal guidelines and anti-terrorist financing. Customers can select to not bear KYC, however they are going to be restricted to the change’s choices. A person is offered a custodial digital pockets, which holds details about their cryptocurrency belongings.

They promote and commerce numerous sorts of cryptocurrency to customers, however they have to adjust to the principles and laws of the monetary system. This makes them regulated entities, and they’re additionally centralized. They’re centralized as a result of they management a person’s pockets by having custody of the non-public key. That implies that the change can freeze an account if deemed non-compliant or in violation of coverage. This prevents customers from shopping for or promoting crypto and withdrawing or transferring their funds. That is very a lot how banks function as nicely.

Fintech firms started creating their very own protocols to supply DeFi companies that might open the market to incomes, staking and liquidity swimming pools. This allowed customers to earn on curiosity from yields that had been typically too good to be true. These protocols provided returns which are a lot increased than any financial institution can provide. These had been provided by firms like Block-Fi, Celsius, Nexo and Abra. They allowed customers to earn curiosity from their cryptocurrency like Bitcoin and Ethereum, by depositing it into their system. These firms take the asset as unsecured collateral, which they will then lend out. Customers earn on derivatives from curiosity on mortgage funds. That is very a lot how banks work, however in a crypto setting.

These firms weren’t DeFi, however CeDeFi or Centralized DeFi. Though they provide devices to DeFi, they don’t seem to be themselves decentralized. These firms are centralized as a result of they management the whole lot on their platform. They’ve custody of their buyer’s account non-public key, which supplies them full management of their digital pockets. They will freeze all withdrawals and transactions, particularly throughout meltdowns.

The collapse started with the autumn of Bitcoin. Since it’s the dominant crypto, the remainder of the market tends to observe its lead. On this case it was a downturn because of the correlation with the inventory market. Traders, largely newbies, had been treating crypto like Bitcoin as threat belongings and had been thus promoting them off on account of financial uncertainty. The market reached a vital degree, and this triggered a sequence of occasions that might collapse CeDeFi.

The following collapse was that of Terra’s stablecoin UST (Terra USD). The stablecoin was pegged to the US Greenback at a 1-to-1 ratio. The pegging was not really backed by any commodity or asset, but it surely was algorithmic in nature. Which means the stablecoin backing is decided by buy of the Terra native token referred to as LUNA. So as to mint UST, LUNA should be burned to again the worth in USD. Through the extra bullish interval of 2021 and 2022, many buyers purchased LUNA and burned it to get UST. The burning eliminated LUNA from circulation, which additionally raises its worth. The catch right here is that customers can then earn from UST by depositing it into the Anchor earn protocol. At one level, it was providing returns of as much as 20% APY. That may be a pink flag proper there for monetary analysts.

Throughout excessive volatility available in the market, UST misplaced its peg to USD. This was due to a financial institution run brought on by panic promoting available in the market. Extra UST was being withdrawn than LUNA being burned. This affected the value of each UST and LUNA. As the costs started to plummet, buyers started to fret, and issues acquired worse. Terra was not in a position to maintain the peg, so LUNA crashed beneath $0 in worth. UST additionally crashed, and this affected large holders, that features CeDeFi firms.

Following the autumn of Terra, the main target was on the funding funds that held UST or LUNA. There have been loads of liquidations throughout the market, as buyers hurried to drag their cash out of UST. Despite the fact that Terra had reserves from their LFG (Luna Basis Guard), it was not sufficient to revive the peg to UST. This may hyper-inflate LUNA as extra UST was being burned again to LUNA tokens. 58% of merchants positioned futures bets on increased LUNA costs regardless of the drop, resulting in $106 million in liquidations when UST dropped to $0.35. The burning of UST to prop up its peg didn’t work as anticipated and as an alternative led to extra LUNA being minted (which drops its worth). The response from exchanges like Binance was to halt LUNA and UST buying and selling.

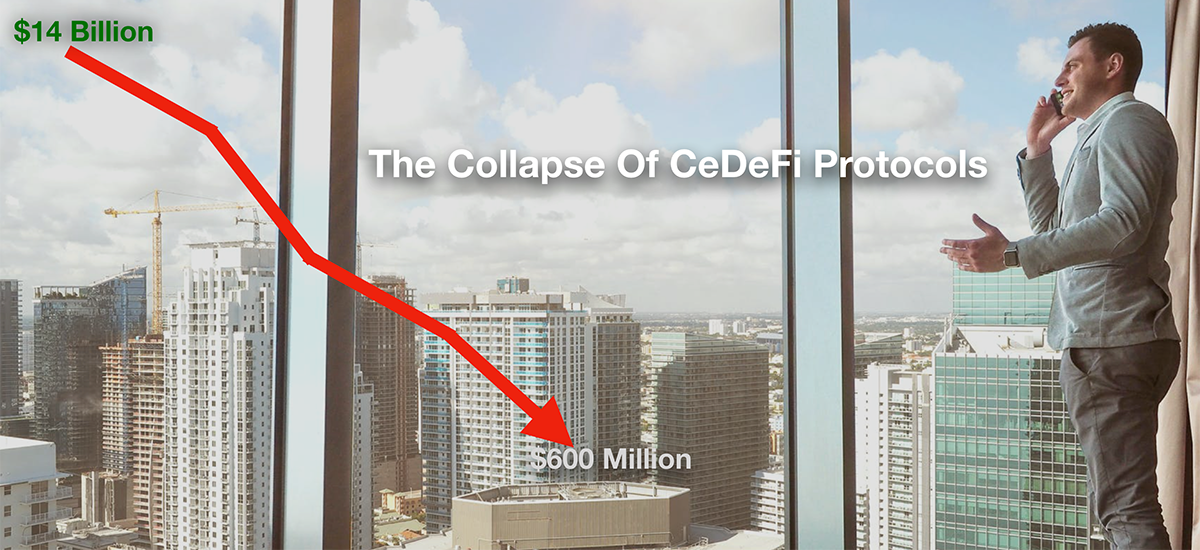

The main target turned to CeDeFi firms after the Terra meltdown. This was as a result of a few of these firms had invested closely into Terra’s UST or LUNA, and these might result in extra worries for buyers. The primary to break down from the UST depeg was the Anchor protocol. The entire worth locked had fallen from $14 Billion to $8.7 Billion as UST worth declined. The protocol has fallen to $600M+ in UST (as of posting).

There was now a liquidity disaster within the crypto market. Liquidations throughout the board drained the market. There have been much less funds on loans, whereas extra customers had been making withdrawals from the system. The warning indicators started to appear with Celsius as extra withdrawals had been being made than capital inflows. In addition they held loads of staked ETH (stETH), which was dropping its peg to ETH as holders started dumping. This led Celsius to halt withdrawals round June 12–13, 2022. Customers wouldn’t be capable to withdraw their belongings or change any crypto.

3AC (Three Arrows Capital) was the subsequent to be scrutinized for insolvency. 3AC has $3 Billion value of belongings beneath administration which incorporates tasks within the crypto area. Because of the crypto crash, 3AC was not in a position to meet the margin calls of undercollateralized loans. They’d additionally taken leveraged positions, in peril of being liquidated. 3AC had misplaced some huge cash from the Terra LUNA crash. $1 million had additionally gone lacking from certainly one of 3ACs buying and selling accounts, and this must be addressed.

Different CeDeFi firms feeling the warmth included Block-Fi, however they haven’t halted withdrawals. They really discovered a lifeline from an FTX bailout. Different CeDeFi firms are holding their floor up to now, however as lengthy the promote offs proceed, they’re on unstable floor. There’s nonetheless a lot uncertainty available in the market, investor anxiousness is reaching excessive concern and bearish sentiments.

So, is it the developer’s fault for creating these protocols that collapse throughout sudden occasions?

It isn’t. As an alternative it’s the individuals behind these CeDeFi protocols who’re extra responsible. The algorithms of their merchandise had been designed for a function. It’s honest to say it was meant to get clients essentially the most yield in curiosity, from their digital belongings. The very fact is that customers who deposit to those protocol’s anticipating big returns are additionally surrendering their belongings to the corporate. The corporate then decides what to do with these belongings. It simply so occurs that these firms could not at all times make the very best selections in threat administration. That is the way it works with CeDeFi lending protocols.

These belongings haven’t any safety in case the corporate experiences issues like insolvency. When the cash stops flowing, there are dangers to liquidation of belongings. The fintechs don’t speak an excessive amount of about this, and as an alternative deal with the ridiculous returns their protocol makes for purchasers. What will not be recognized to customers is that their belongings are getting used as collateral to get these returns from different protocols. These may be decentralized yield farming protocols like Yearn or Aave, or invested into incomes protocols like Anchor on the Terra community.

The usage of buyer’s digital belongings opens them up for dangers that can’t be mitigated within the occasion of a financial institution run or financial downturns. CeDeFi firms have confronted scrutiny for not following monetary guidelines that regulators just like the SEC have put forth. These deposits should not absolutely secured, and due to this fact there isn’t a full obligation by the fintechs to ensure their security to clients. As an alternative, they provide assurances of safety via sensible advertising that goals to get the shopper’s belief in return for his or her belongings. A number of the fintechs are actually following these guidelines to safe buyer’s belongings, however there have been no enforcements prior to now.

Maybe it’s time to say the quiet half out loud or the main points that nobody needs to debate about CeDeFi. Let’s enumerate them:

– CeDeFi will not be decentralized, these are centralized firms that may management person belongings. They censor your transactions, freeze your account, halt withdrawals and even liquidate your crypto.

– CeDeFi are like banks and lending establishments typically. They take your deposited crypto belongings and lend it to different establishments. You make a yield on curiosity from mortgage funds, at increased than regular charges as a result of there are much less intermediaries to cope with in crypto. Which means much less middle-men get a reduce, granting extra to the customers.

– When depositing your crypto to CeDeFi protocols to earn, you’re giving the corporate your belongings as an unsecured mortgage. You’re lending to the corporate to lend out your belongings as collateral for funding. Since it’s unsecured, there isn’t a assure the asset may be recovered within the occasion of a chapter or different unlucky occasion. It isn’t FDIC coated like in conventional monetary programs, so this can be a threat the person should perceive.

To ensure that CeDeFi to regain confidence available in the market, some issues want to vary. These protocols in comparison with actual DeFi have collapsed. Maker DAO, which is a decentralized lending protocol, has held up via this meltdown. It’s because they don’t observe the identical observe as CeDeFi firms. Maker DAO points its stablecoin DAI, which is backed by a commodity that’s overcollateralized to cowl any conditions of non-payment of loans. DeFi protocols observe a market pushed strategy that can’t be managed by any group or particular person.

The meltdown has led to calls for brand new laws on the crypto market, focusing on the fintechs who’re CeDeFi firms. Whereas that is meant to offer extra client safety, it may also be to revive religion on this market. Proper now, there’s a whole lack of confidence after withdrawals had been halted, and plenty of customers are fearing the worst. This has led to customers on different CeDeFi platforms to rapidly withdraw their belongings.

What occurred here’s a cautionary story as soon as once more. You may have these monetary geniuses coming into a very new monetary system that goals to ship increased yields than conventional monetary programs. They rapidly poured capital to spend money on these DeFi tasks, however operated by a centralized firm. You will get increased returns as a result of that was what the system was programmed to do, however relating to extremes in market situations, they may not regulate to stop a collapse. A few of these fintechs engaged in over leveraged actions, not foreseeing the downturn in market situations. They can provide excessive returns on rates of interest, however by no means handle to clarify how they had been going to maintain these funds on returns.

It’s higher to have some type of regulation for CeDeFi to a minimum of mitigate some (if not all) of the catastrophe that occurs when markets crash. True DeFi protocols at this level seem much less dangerous, since they don’t forestall withdrawals and truly work in response to the free market. CeDeFi may be managed by just a few decision-makers, who can shut down the community at any time when they like, stopping customers from accessing their belongings. Regulation also needs to embody requiring extra transparency on the place customers’ belongings are getting used to discourage unhealthy religion practices from these fintechs.

These occasions have given a nasty identify to DeFi, though it was the CeDeFi fintechs that brought on the issue. Customers are studying that it’s higher to have custody of their very own belongings (e.g. Your Keys, Your Cash) moderately than granting custody to a 3rd social gathering. Even when it doesn’t earn curiosity, a minimum of it stays of their possession and can’t be liquidated. This also needs to sign to fintechs to assessment their technique in DeFi to offer extra safety to clients and provide practical returns which are sustainable. Proper now, CeDeFi must construct extra belief and confidence with their clients, or else time to pack it up.

[ad_2]

Source link

{kind=link}