[ad_1]

krblokhin/iStock Editorial through Getty Photographs

Raytheon Applied sciences (NYSE:RTX) has been among the many few high-profile vivid spots in a dismal 12 months for the inventory market. Shares of the aerospace and protection conglomerate have held in optimistic territory whereas many different family names have plummeted for the reason that finish of 2021.

RTX has obtained assist from its dividend and gained consideration amid heightened geopolitical tensions since Russia invaded Ukraine again in late February. Given these circumstances, does the inventory stay a purchase headed into the second half of the 12 months, as buyers hunt for return amid rising rates of interest and shaky economic system?

Holding Power in a Weak Market

RTX has stumbled like most of Wall Road over the previous few buying and selling classes. Nonetheless, the inventory stays optimistic for the 12 months as an entire, rising by nearly 6% in 2022.

These returns far outstrip the broader markets. The S&P 500 has dropped almost 22% for the 12 months, whereas the Nasdaq has fallen greater than 30%.

The assist for RTX has come largely on account of its place as a high protection contractor. Geopolitical tensions have escalated within the wake of Russia’s assault on Ukraine.

This has been underlined by latest contract wins. Raytheon was awarded a $624.6M contract for the procurement of Stinger missiles and related gear. Moreover, RTX inked a $217.12M Navel contract.

Is RTX a Purchase?

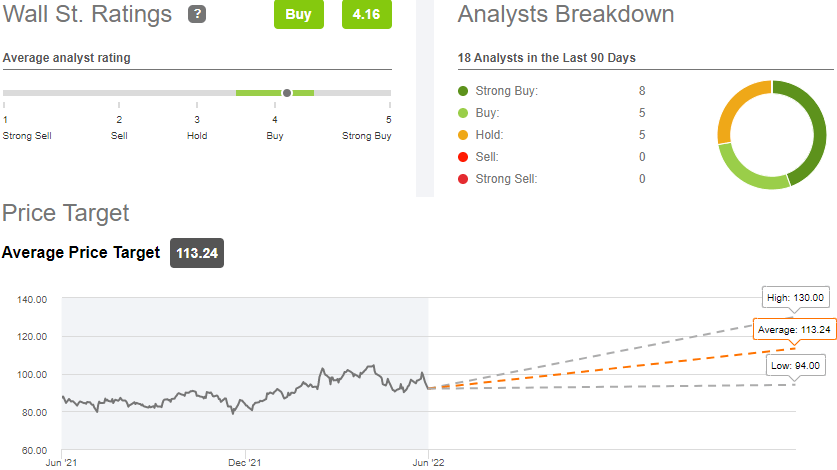

Wall Road takes a comparatively bullish view of RTX. If the 18 analysts surveyed by Looking for Alpha, almost 75% labeled the agency as a Robust Purchase or Purchase. Eight label RTX as a Robust Purchase and 5 classify the inventory as a Purchase. In the meantime, the remaining 5 gave RTX a Maintain ranking.

Furthermore, the inventory trades close to $91 a share, and analysts record Raytheon with a median worth goal of $113.24. The bottom goal estimate is $94 a share whereas the best goal is listed at $130.

See the breakdown under:

Looking for Alpha’s Quant Rankings give the inventory an much more upbeat evaluation. These grades, primarily based on quantitative measures, see the inventory as an A+ in terms of profitability and an A with reference to momentum.

There are some factors of concern, nonetheless. The Quant Rankings subject a C+ for the agency’s development and a D relating to the inventory’s valuation.

For a deeper dive into the inventory, Looking for Alpha contributor Librarian Capital holds a bullish opinion on RTX, praising the agency’s stable Q1 outcomes again in April, which featured EBIT up almost 19% from final 12 months.

Taking a extra impartial stance, fellow SA contributor Envision Analysis sees RTX as a Maintain, believing it’s pretty and totally valued regardless of it exhibiting robust fundamentals.

[ad_2]

Source link

{kind=link}