[ad_1]

Uncertainty has been the secret in 2022. A mixture of detrimental macro developments – a slowing international economic system, the geopolitical ramifications following Russia’s invasion of Ukraine and – probably most of all – the prospect of the Fed critically tightening its financial coverage to fight inflation – have all been weighing closely on buyers’ minds.

That doesn’t essentially imply there aren’t good alternatives to reap the benefits of proper now. The analysts at banking large Goldman Sachs have pinpointed two names which have lately outperformed market expectations and which they consider are set to surge forward even within the face of the unhospitable present atmosphere – by the order of 40% or extra.

We ran each tickers by the TipRanks database to see what the remainder of the Avenue has in thoughts for the pair. Let’s check out the findings.

Pure Storage (PSTG)

The primary inventory on Goldman Sachs’ radar is Pure Storage, a supplier of assorted information storage merchandise. The corporate’s flash-based options come each in software program and {hardware} kind and are utilized in information facilities. The corporate started by utilizing third-party solid-state drives (SSDs) for its storage options. Nevertheless, its personal proprietary {hardware} quickly changed these SSDs and the corporate additionally introduced into the market built-in deduplication, compression, and synthetic intelligence software program to assist companies preserve house and arrange their gadgets correctly.

Pure Storage has shaped a robust partnership with Meta, having assisted within the growth of the preliminary model of its AI analysis infrastructure in 2017. Since then, the pair have continued working collectively and earlier this 12 months the 2 started a collaboration on Meta’s new AI Analysis SuperCluster (RSC), which Meta claims would be the quickest AI supercomputer on the earth.

Like most tech shares, Pure has discovered 2022 exhausting going however that hasn’t stopped the corporate from delivering the products in its newest quarterly report.

In F1Q23, income rose by 50.3% year-over-year to achieve $620.4 million, handily beating the $521.74 million Wall Avenue anticipated. Equally, on the bottom-line, adj. EPS of $0.25 got here in effectively above the $0.05 consensus estimate. The corporate delivered on the outlook too, anticipating income of roughly $635 Million in FQ2 vs. consensus at $604.64 million. For the total 12 months, gross sales are anticipated to achieve $2.66 Billion. Analysts had that determine at $2.59 billion.

Together with the corporate’s exemplary execution, it’s the Meta collab which informs Goldman analyst Rod Corridor’s bullish thesis.

“We see this Meta alternative as a robust income tailwind for Pure trying ahead in FY’23. We additionally see ongoing sturdy outcomes as a sign that Pure’s merchandise are gaining an growing following amongst enterprise and repair supplier clients,” the analyst opined. “At this level we see Pure’s provide administration as superior to most different firms in our protection within the IT {hardware} space.”

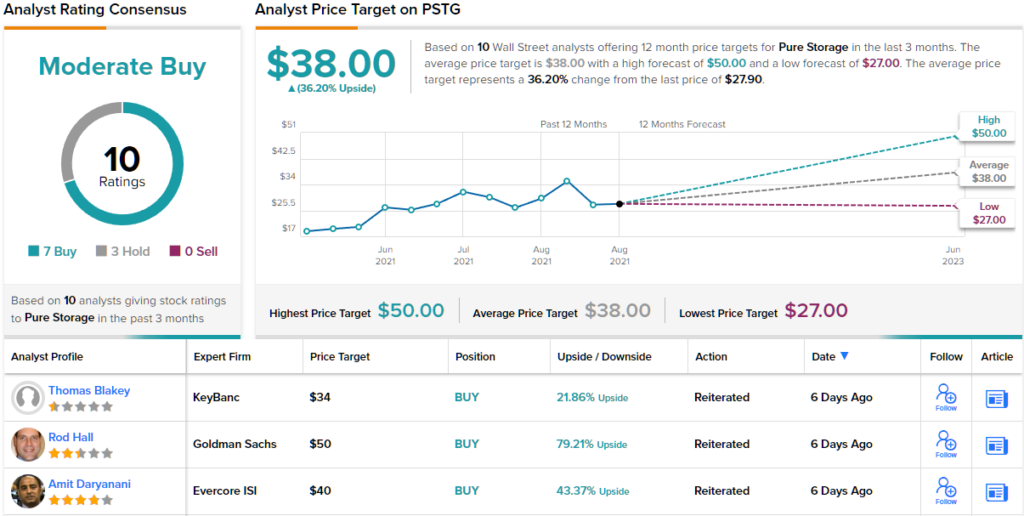

The bullish feedback underpin Corridor’s Purchase score whereas his $50 worth goal makes room for one-year good points of 79%. (To observe Corridor’s observe report, click on right here)

General, PSTG has attracted a complete of 10 analyst evaluations lately, together with 7 Buys and three Holds for a Reasonable Purchase consensus score from the Avenue. PSTG shares are priced at $27.90 and have a mean worth goal of $38, giving the inventory a 36% upside on the one-year time-frame. (See PSTG inventory forecast on TipRanks)

Lululemon Athletica (LULU)

From tech we are going to pivot over to a completely completely different sector. Everybody is aware of Lululemon – the athleisure specialist. The corporate acquired its beginnings in 1998 as a yoga pants and different yoga clothes retailer, however has since developed to incorporate athletic put on, way of life garments, private care merchandise and all method of equipment. Lululemon now has over 570 shops unfold throughout the globe whereas it has additionally constructed a robust on-line presence. In attire, the corporate has been rated because the world’s fourth most beneficial model.

Lululemon was one of many Covid period stars as folks stayed at house and slipped into extra snug put on, whereas the corporate even managed to beat the closure of bodily shops by shifting gross sales on-line. Whereas not proof against the market’s total downturn, Lululemon seems to have managed effectively within the face of recent challenges, particularly the provision chain points which have impacted so many in current instances. This was evident within the firm’s newest earnings report – for F1Q22.

Lululemon generated income of $1.6 billion, a 32% enhance on the identical interval a 12 months in the past, whereas diluted EPS hit $1.48. Each had been above the analysts’ forecast of $1.55 billion and $1.43, respectively. There was extra excellent news for the outlook. For FQ2, Lululemon sees income coming within the vary between $1.750 billion to $1.775 billion, above consensus of $1.73 billion. And the corporate additionally raised its income and EPS outlook for the total 12 months.

Surveying the print, Goldman Sachs analyst Brooke Roach is totally impressed. She writes, “We come away from the quarter with elevated conviction in LULU’s sturdy model engine fueled by innovation. Whereas trade value pressures are weighing on margin flow-through (the place airfreight pressures have lowered full 12 months margin outlook modestly), we proceed to see this idiosyncratic development story as well-positioned to navigate a tricky backdrop as the corporate has significant pricing energy, sturdy client connection, and fewer publicity to inflating AUCs (common unit value).”

Accordingly, Roach charges the inventory a Purchase, backed by a $456 worth goal. Going by this goal, shares are anticipated to climb 48% larger over the one-year timeframe. (To observe Roach’s observe report, click on right here)

Wanting on the consensus breakdown, the vast majority of analysts are bullish on LULU’s prospects, too; 19 Buys and seven Holds add as much as a Reasonable Purchase consensus score. The common worth goal of $409.69 suggests upside of ~34% within the 12 months forward. (See Lululemon inventory forecast on TipRanks)

To search out good concepts for shares buying and selling at enticing valuations, go to TipRanks’ Finest Shares to Purchase, a newly launched software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is extremely essential to do your personal evaluation earlier than making any funding.

[ad_2]

Source link